Carbon Emissions Explained

Why Understanding the Basics Is More Complex Than It Seems

In most boardrooms today, carbon emissions are treated as a measurable externality—something that can be calculated, reported, and eventually reduced. The prevailing assumption is deceptively simple: quantify emissions, apply reduction strategies, and demonstrate compliance. But this assumption rests on a fragile conceptual foundation.

What appears to be a straightforward environmental metric is, in reality, a layered system of interdependent concepts that shape how organizations interpret risk, assign cost, and make operational decisions. Before any measurement system, regulation, or technology can be meaningfully applied, the core concepts themselves must be understood with precision—and, more importantly, with skepticism.

This is where most organizations fail. Not because they lack tools, but because they operate on incomplete mental models.

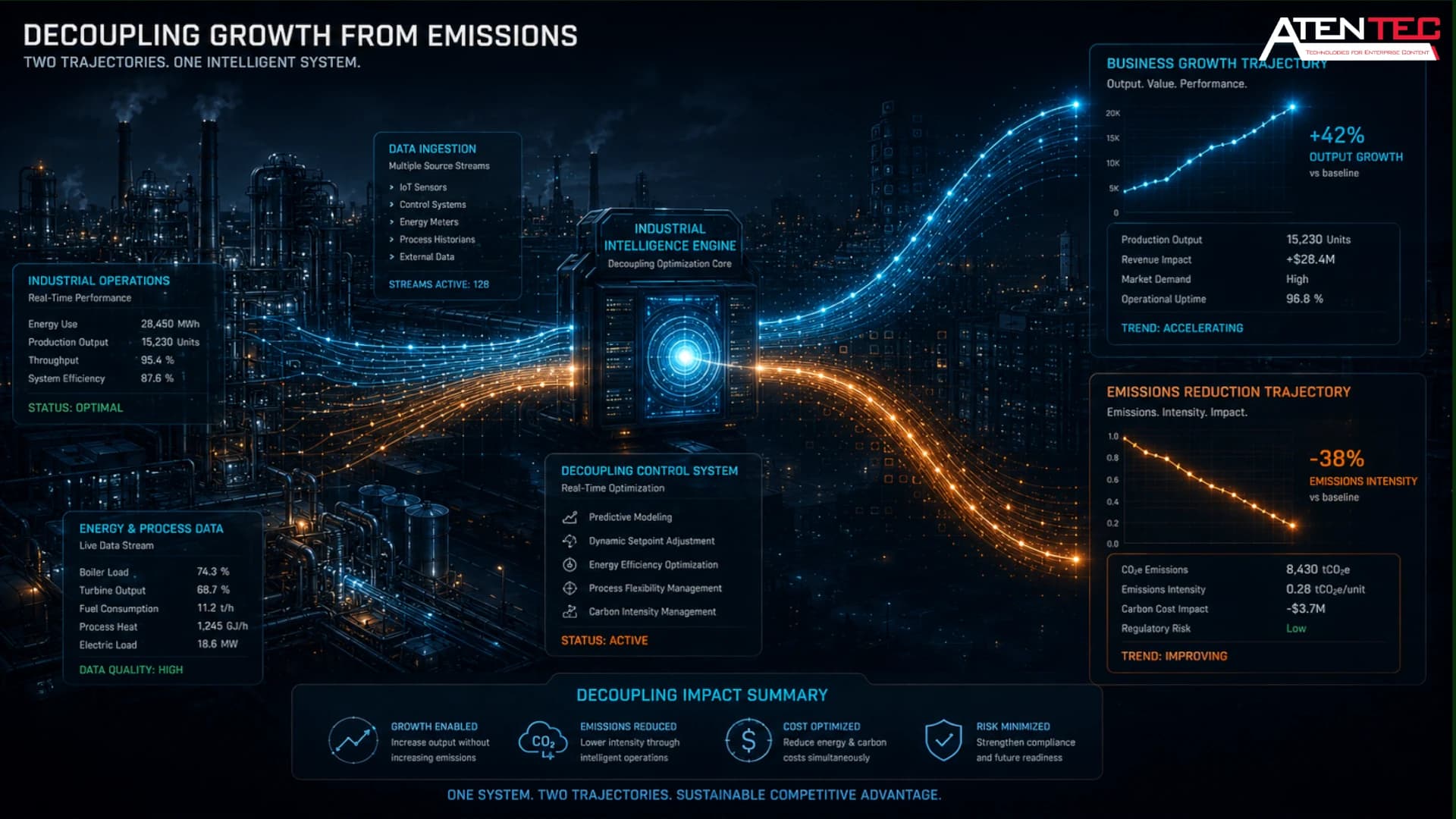

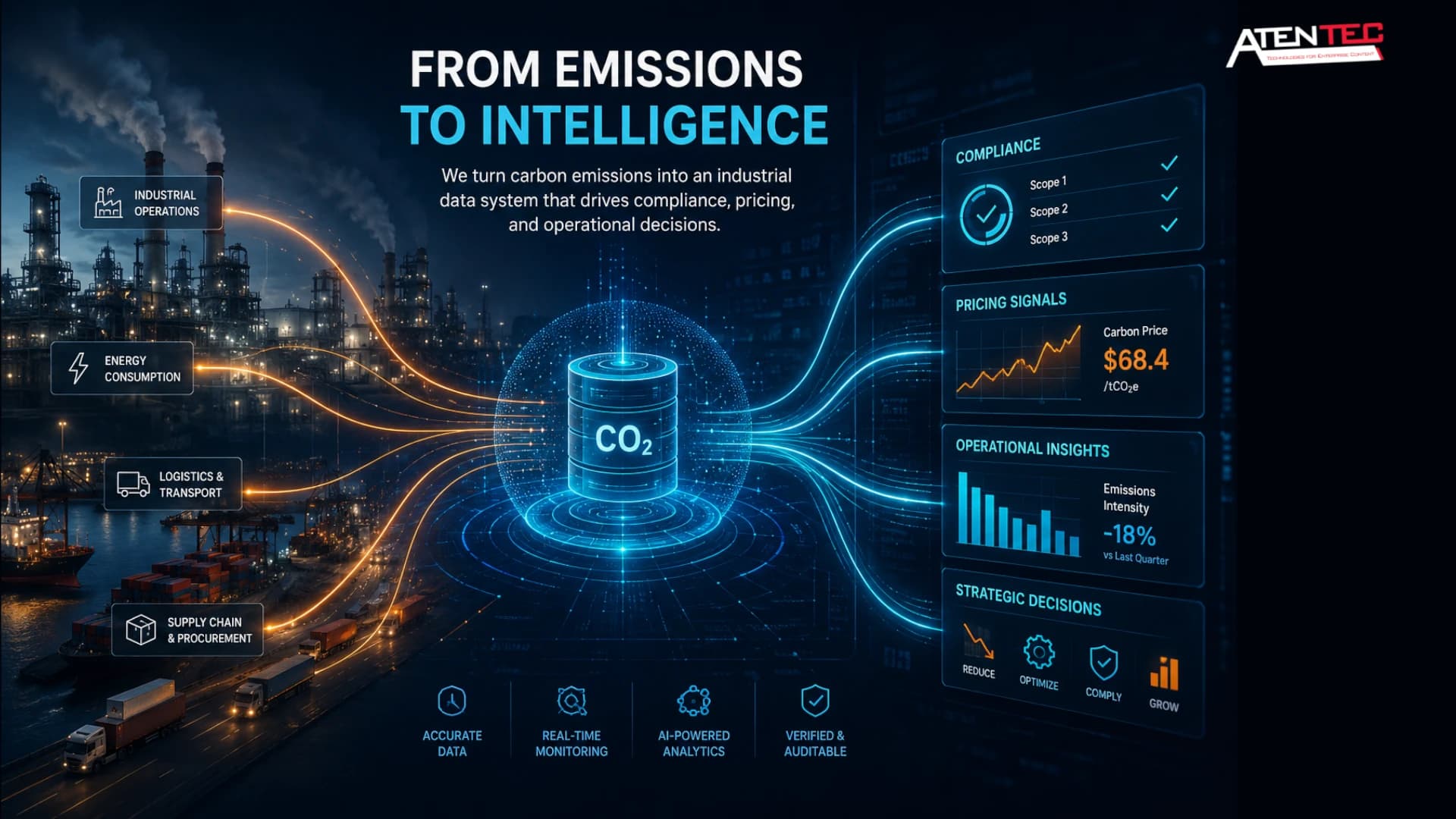

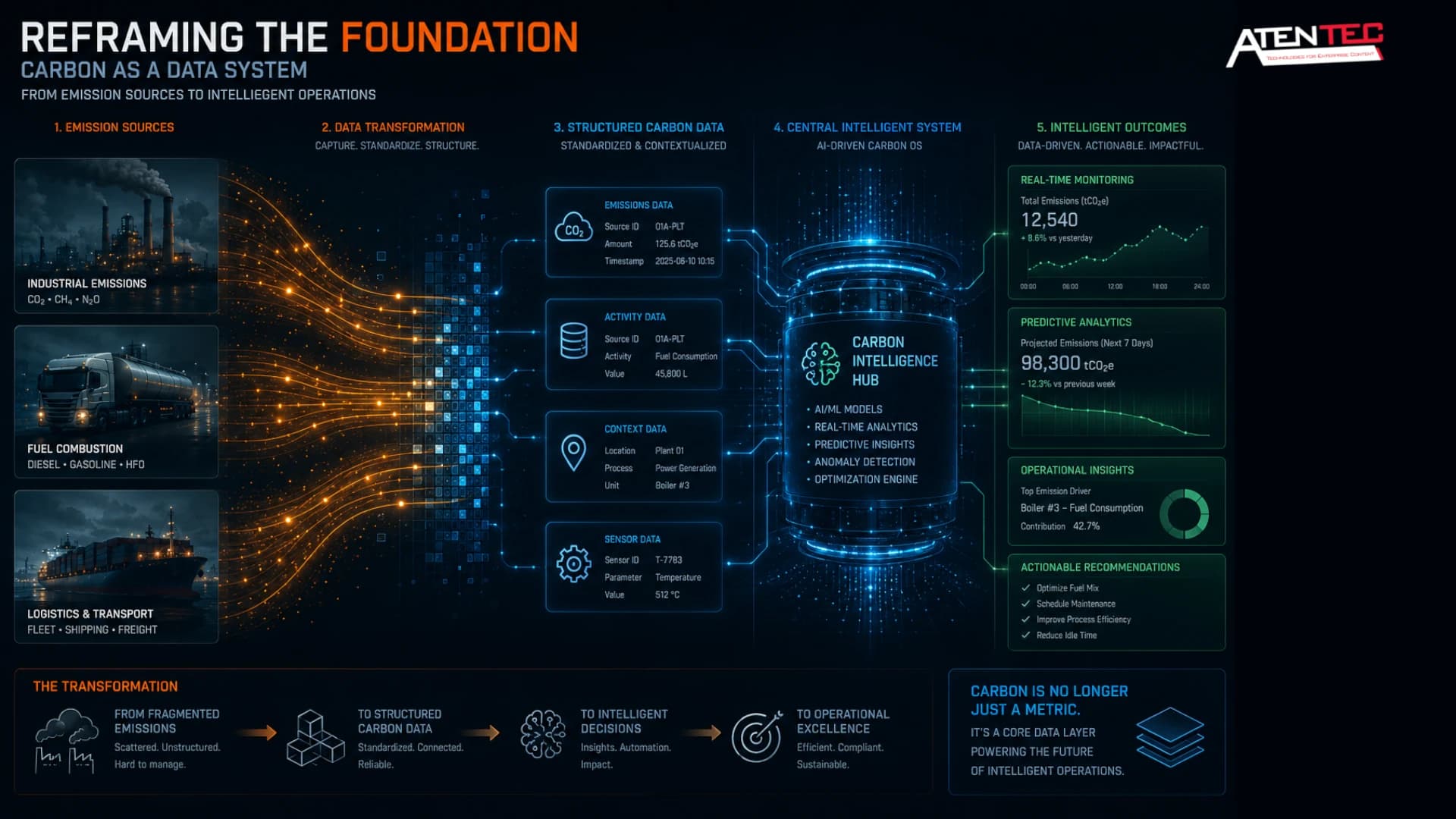

At AtenTEC, the positioning is explicit: we turn carbon emissions into an industrial data system that drives compliance, pricing, and operational decisions. That transformation cannot happen without reconstructing how these core concepts are understood.

Carbon Footprint: The Illusion of a Single Number

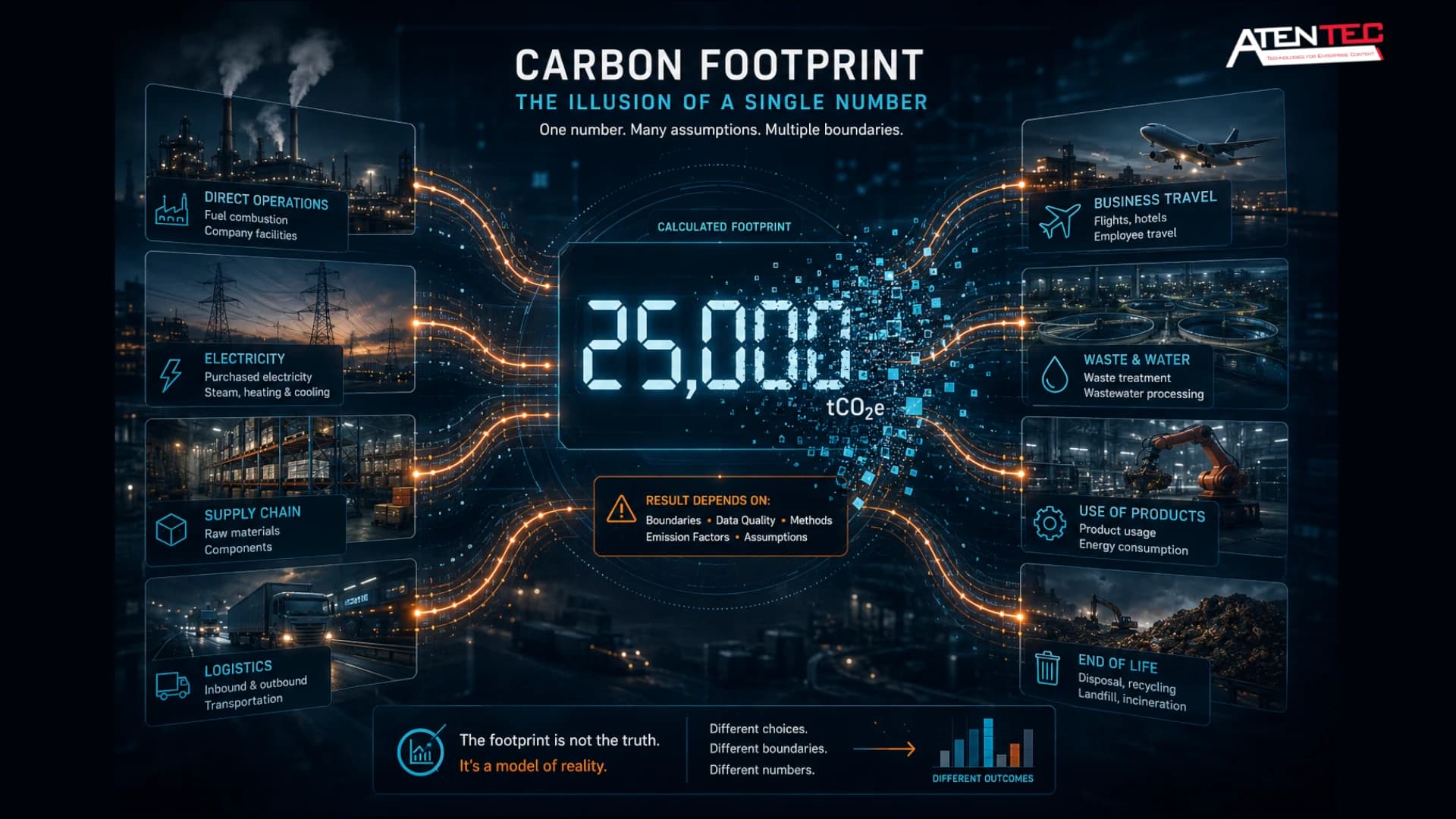

The term “carbon footprint” is often used as if it represents a definitive measurement—a fixed number that reflects the environmental impact of an entity. In practice, it is neither fixed nor singular.

A carbon footprint is a constructed metric. It aggregates emissions across activities, processes, and boundaries that are often arbitrarily defined. Two companies with identical operations can report different footprints simply because they draw their system boundaries differently or rely on different data assumptions.

Consider a hospitality operator in a coastal tourism hub. Its reported carbon footprint may include direct fuel usage and electricity consumption. But what about outsourced laundry services? Imported food supply chains? Guest transportation? Each inclusion or exclusion fundamentally alters the footprint. The number itself becomes less important than the methodology behind it.

This is where the misconception lies: the footprint is not the truth—it is a model of reality. And like any model, it is shaped by assumptions, constraints, and data availability.

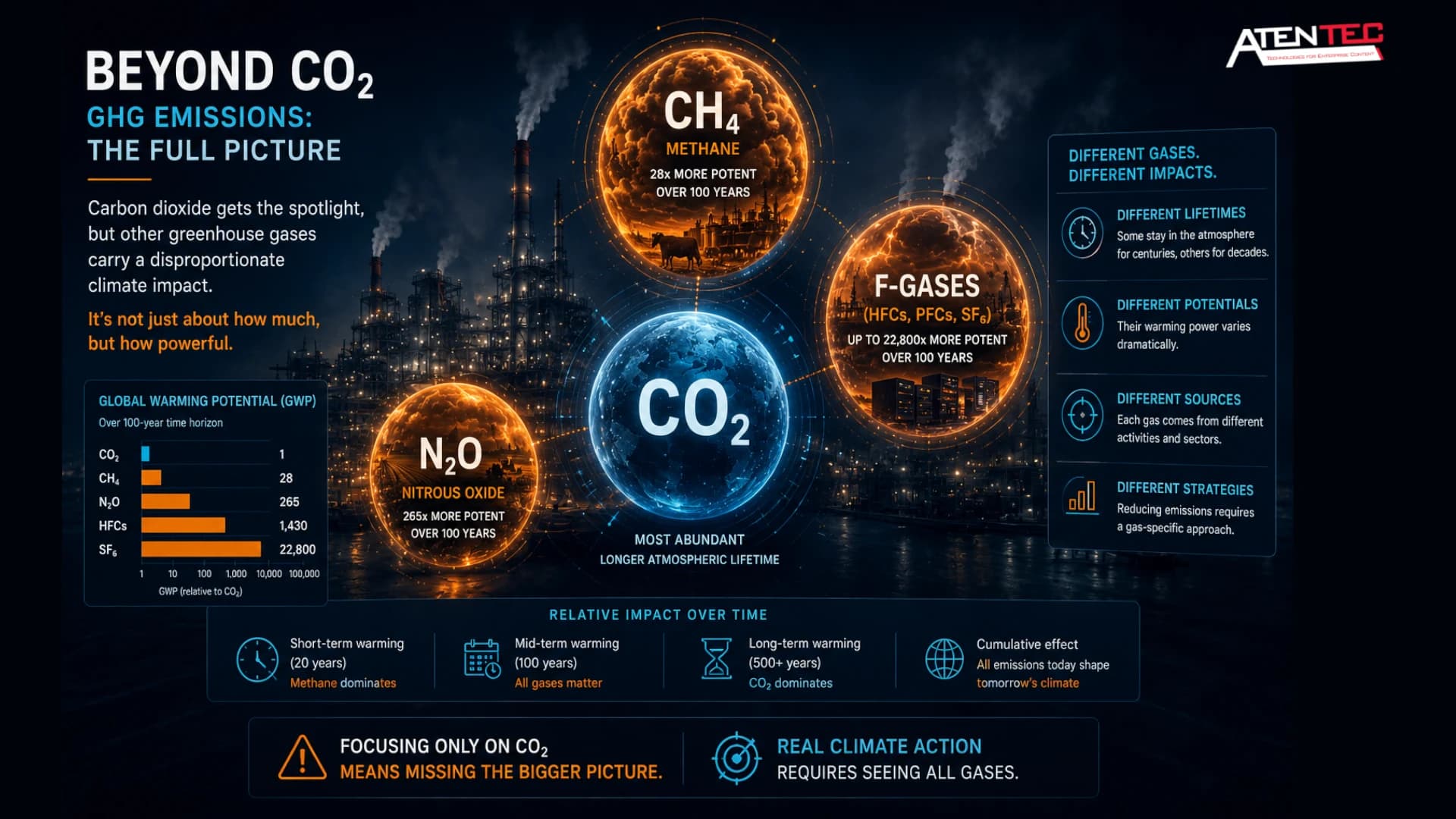

GHG Emissions: Why CO₂ Is Only Part of the Story

Carbon dioxide dominates public discourse, but it represents only one component of a broader category: greenhouse gas emissions. Methane, nitrous oxide, and fluorinated gases each have significantly different global warming potentials and temporal behaviors.

Reducing emissions to “CO₂” simplifies communication but distorts decision-making. Methane, for instance, has a much higher warming potential over a shorter timeframe. In sectors like waste management or agriculture, ignoring methane leads to a severe underestimation of climate impact.

In industrial contexts, this distinction becomes operationally critical. A logistics company optimizing fuel efficiency might reduce CO₂ emissions while overlooking refrigerant leaks in its cooling systems—emissions that could have a disproportionately higher climate impact.

The implication is clear: emissions are not homogeneous. Treating them as such introduces systemic bias into both reporting and strategy.

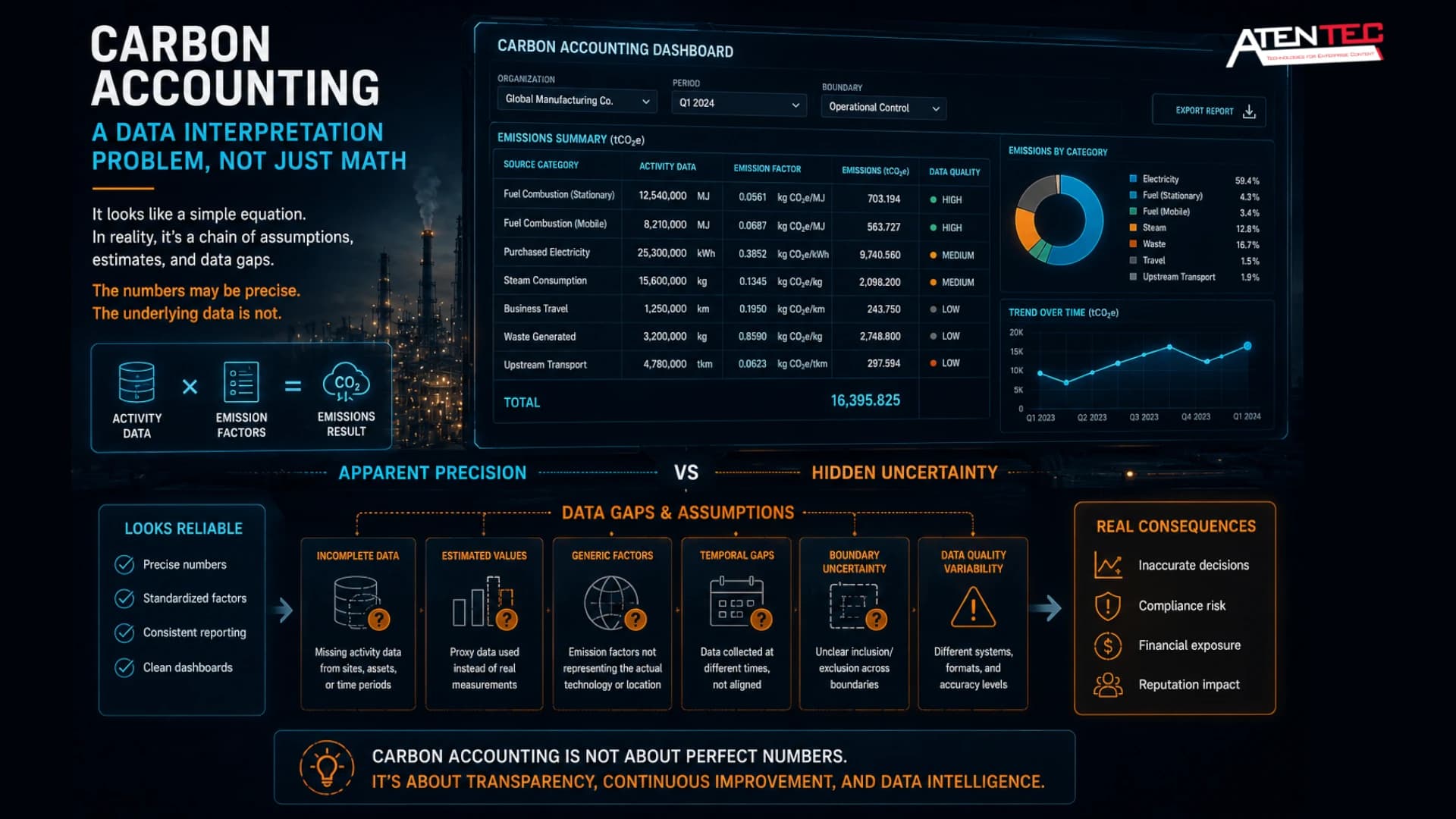

Carbon Accounting: A Data Interpretation Problem Disguised as Mathematics

At its core, carbon accounting is often presented as a simple equation: activity data multiplied by emission factors. This framing suggests determinism and precision. In reality, carbon accounting is an exercise in data interpretation under uncertainty.

Activity data is rarely complete. Emission factors are often generalized averages derived from datasets that may not reflect local conditions or specific technologies. Temporal mismatches, data gaps, and estimation techniques introduce layers of variability that are rarely visible in final reports.

Take the example of a fleet operator calculating emissions from fuel consumption. The emission factor applied may be based on regional averages, while actual fuel quality, engine efficiency, and driving conditions vary significantly. The resulting number appears precise but carries embedded uncertainty that is not explicitly communicated.

This is why carbon accounting should not be treated as a compliance checkbox. It is closer to financial forecasting than bookkeeping—requiring judgment, assumptions, and continuous refinement.

Carbon Intensity: The Metric That Changes Decisions

If carbon footprint answers the question “how much,” carbon intensity answers “relative to what.” It measures emissions per unit of output—per product, per kilometer, per revenue unit.

This shift from absolute to relative metrics is where carbon begins to influence real business decisions.

A manufacturing facility may increase its total emissions while simultaneously reducing its carbon intensity by improving production efficiency. From a regulatory standpoint, this may still be problematic. But from an operational perspective, it signals improved performance.

Conversely, a company can reduce total emissions by scaling down operations, while its carbon intensity remains inefficient. Without understanding intensity, decision-makers risk optimizing for the wrong objective.

In pricing strategies, carbon intensity becomes even more critical. As mechanisms like carbon taxes and border adjustment policies emerge, the cost of emissions is increasingly tied to output efficiency. Products are no longer evaluated solely on cost and quality, but on embedded carbon per unit.

From Concepts to Systems: Where Misunderstanding Becomes Risk

Individually, each of these concepts—carbon footprint, greenhouse gas emissions, carbon accounting, and carbon intensity—appears manageable. Together, they form a conceptual system that determines how emissions are perceived, measured, and acted upon.

Misunderstanding this system leads to predictable failures. Companies invest in reporting tools without questioning data quality. They commit to reduction targets without understanding baseline uncertainty. They benchmark against competitors without aligning methodologies.

The result is not just technical inefficiency—it is strategic misalignment.

When carbon is treated as a reporting obligation, it remains disconnected from core business functions. But when it is understood as a data system, it begins to influence procurement decisions, operational design, pricing models, and risk management frameworks.

Reframing the Foundation

The purpose of revisiting these core concepts is not educational in the traditional sense. It is corrective.

The market does not suffer from a lack of information about carbon emissions. It suffers from overconfidence in simplified interpretations. The danger is not ignorance—it is false clarity.

By challenging the apparent simplicity of these foundational ideas, a different perspective begins to emerge: carbon is not an environmental metric layered on top of business operations. It is a data dimension embedded within them.

And once that shift happens, the conversation moves from “how much do we emit?” to “how do emissions shape how we operate, compete, and grow?”

That is the threshold between awareness and intelligence—and it is where the rest of the carbon system begins.

Where This Leads Next

What we have done here is not to define carbon emissions in the traditional sense, but to deliberately unsettle the way they are usually understood. The concepts may look familiar—carbon footprint, GHG emissions, carbon accounting, carbon intensity—but once examined closely, they stop behaving like static definitions and start revealing themselves as variables inside a much larger system.

And that is precisely the point.

Because once these core ideas are no longer taken at face value, the next layer of questions becomes unavoidable. If the footprint is constructed, how exactly is it measured? If emissions data is uncertain, how do companies report it with confidence? If intensity changes decisions, how do regulations price that difference? And if most emissions sit outside direct control, how can supply chains be made visible?

This is where the broader carbon domain begins to unfold—not as isolated topics, but as a connected architecture.

In the next set of articles, we will move deliberately through that architecture.

We will start with measurement systems, where the gap between theoretical accuracy and real-world data becomes impossible to ignore. From there, we will examine how regulation transforms emissions into legal and financial exposure, before shifting to the supply chain layer, where most companies discover that their largest carbon risks are the least controllable.

Only then does the role of technology become clear—not as a reporting tool, but as an operational necessity. And finally, we will reach the financial layer, where carbon stops being an environmental concern and becomes a priced asset, a liability, and in some cases, a competitive advantage.

Each concept introduced here will be unpacked individually, not as definitions, but as decision frameworks.

Because the objective is not to know what carbon emissions are.

The objective is to understand how they behave inside your business.

And that is exactly where our work begins.

You can know more about I-DNTITI “𝗜-𝗗𝗡𝗧𝗜𝗧𝗜: 𝗜𝗻𝘁𝗲𝗿𝗮𝗰𝘁𝗶𝘃𝗲 𝗗𝗶𝗴𝗶𝘁𝗮𝗹-𝗵𝘂𝗯 𝗳𝗼𝗿 𝗡𝗲𝘁-𝘇𝗲𝗿𝗼 𝗧𝗿𝗮𝗻𝘀𝗶𝘁𝗶𝗼𝗻 𝗮𝗻𝗱 𝗜𝗻𝗰𝗹𝘂𝘀𝗶𝗼𝗻 𝘁𝗼𝘄𝗮𝗿𝗱𝘀 𝗧𝗿𝗮𝗻𝘀𝗳𝗼𝗿𝗺𝗮𝘁𝗶𝘃𝗲 𝗜𝗻𝗱𝘂𝘀𝘁𝗿𝘆” program, and follow this article updates for the detailed articles.

│ ├── carbon footprint (Up next)

│ ├── GHG emissions (Upcoming)

│ ├── carbon accounting (Upcoming)

│ └── carbon intensity Upcoming

You can go deeper into our becoming articles plan from Our Core Framework: Understand how we map this system from From Basic Concepts to Financial Impact.

Because the real question is no longer:

How much do we emit?

But rather:

How do we use emissions data to drive better decisions?

,And that is where the real transformation begins.